What is Blockchain and How Is It Radically Transforming the Economy and Industry?

I’ve always been fascinated by systems that challenge the status quo. And few technologies have done that as dramatically as blockchain.

This isn’t just about Bitcoin prices or cryptocurrency hype. It’s about a fundamental shift in how we think about trust, ownership, and value transfer in the digital age. Blockchain is the underlying technology that makes it possible — a way to record and transfer information transparently and securely without central intermediaries.

To understand why that matters, we need to go back to the beginning. Not the beginning of blockchain, but the beginning of money itself.

The Problem Money Solved (and Created)

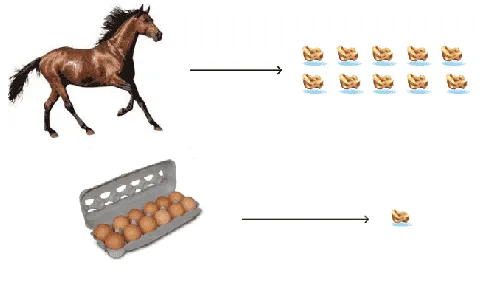

Think about early human exchange. I have eggs, you have a horse. I want your horse. How many eggs is that worth?

This is the fundamental challenge of barter: establishing fair exchange rates between completely different things. One egg versus one horse — clearly not equivalent. But how do you calculate it without a common reference point?

Humanity’s solution was brilliant: gold. A scarce, attractive, durable natural resource that everyone valued. Gold became the universal reference — the standard against which everything else could be measured.

Let’s use a simple example (borrowed from the movie The Contestant). A farmer wants to trade eggs for a horse. Through market dynamics, people established that:

- 1 gold nugget = 1 comb of eggs

- 1 horse = 10 gold nuggets

So through basic math: 120 eggs = 1 horse.

Gold became the first currency — a universal medium of exchange.

But gold had a problem: weight. Imagine carrying sacks or cartloads of gold to do business. Inefficient. Insecure. Impractical.

So people started leaving their gold with goldsmiths for safekeeping. The goldsmith would give them a paper receipt as proof. And here’s where it gets interesting: people started trading those receipts instead of the actual gold.

That’s how paper money was born — a claim on gold, not the gold itself.

Then goldsmiths discovered something clever: they didn’t need to keep all the gold in their vaults. As long as people trusted they could redeem their receipts, goldsmiths could issue more receipts than they had gold. This is called fractional reserve banking — and it’s still how modern banks work.

Over time, the link to gold disappeared entirely. Money became backed not by metal, but by faith and trust in the issuing institution.

The Rise of Trust Intermediaries

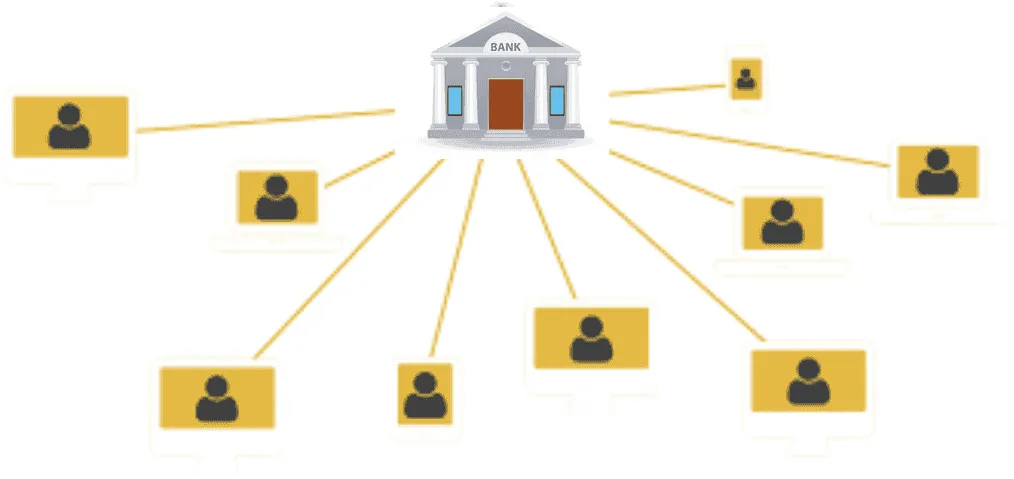

Fast forward to today. Global commerce depends on banks and financial institutions to facilitate transactions between strangers. They act as trusted third parties — intermediaries who assume risk so buyers and sellers don’t have to.

This creates a centralized trust model. We deposit money in banks. We trust them to hold it, transfer it, and keep records. In return, we pay fees, accept delays, and surrender control.

But centralized systems have inherent weaknesses:

- Single points of failure — technical or malicious

- Corruption and bad actors — a small percentage of fraud is considered “acceptable”

- Lack of transparency — we trust the institution to be honest

And then 2008 happened.

The 2008 financial crisis exposed the dangers of centralized financial power. Greed and reckless management of mortgage bonds crashed the global economy. Lehman Brothers collapsed. Major institutions needed bailouts. Trust in the financial system cratered.

It became clear: we needed an alternative.

Bitcoin: A Peer-to-Peer Electronic Cash System

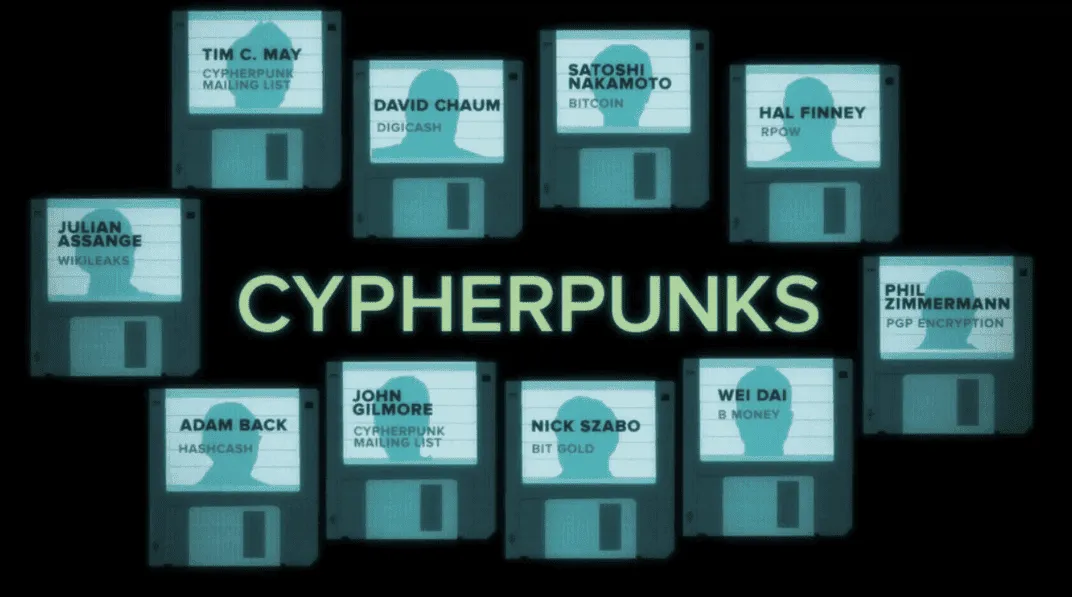

The idea of money without central control had been around for a while. The Cypherpunks — a movement obsessed with privacy and cryptography — had been exploring it for years. But no one had built a practical system.

Then, on October 31, 2008 — at the height of the financial crisis — an anonymous person (or group) published the famous Bitcoin whitepaper under the pseudonym Satoshi Nakamoto.

Satoshi’s paper described a purely electronic version of cash — a system where you could exchange value directly, peer-to-peer, without needing a bank or payment processor in the middle.

Shortly after, Satoshi built the first working implementation of Bitcoin. On January 11, 2009, he sent the first transaction to collaborator Hal Finney: 10 BTC to test the network.

At the time, Bitcoin had no real-world value. But on May 22, 2010, a developer named Laszlo Hanyecz posted on a Bitcoin forum offering 10,000 BTC to anyone who would deliver two pizzas to his house.

Someone accepted. The first real-world Bitcoin transaction happened.

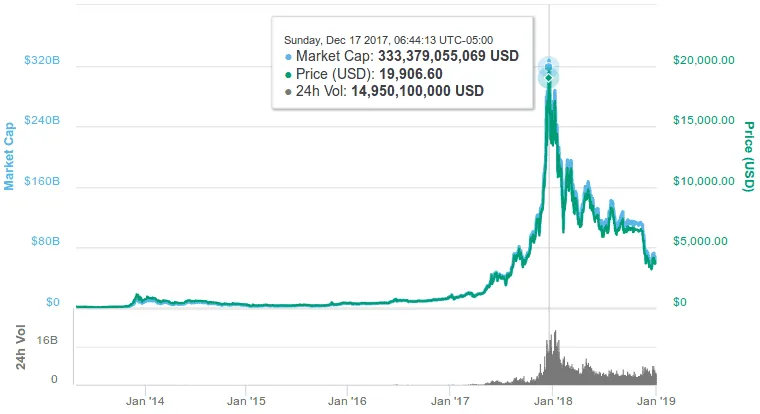

Those 10,000 BTC? At Bitcoin’s 2017 peak of nearly $20,000 per coin, they were worth $200 million. Quite possibly the most expensive pizzas in history.

Bitcoin became a reliable, cheap way to exchange value globally — especially useful for avoiding the high fees charged by traditional intermediaries.

What Makes Bitcoin Different

Here’s what stood out to me about Bitcoin when I first studied it:

Security — Impossible to counterfeit or duplicate, thanks to sophisticated cryptography.

Distributed system — Instead of one central server, Bitcoin runs on a network of computers (nodes) around the world. No single point of control or failure.

No intermediaries — Transactions happen peer-to-peer. There’s no bank in the middle. Instead, the network itself validates transactions through proof of work.

No central authority — Bitcoin doesn’t belong to any government or country. It’s borderless.

Strong ownership — Your Bitcoin is 100% yours. No one can freeze your account or seize your funds.

Irreversible transactions — Once confirmed, transactions can’t be reversed. This prevents the double-spending problem — spending the same digital token twice.

Anonymous (or pseudonymous) — You don’t need to reveal your identity to transact, preserving privacy.

How Blockchain Actually Works

So how does Bitcoin prevent double-spending without a central authority? That’s where blockchain comes in.

The Double-Spending Problem

Digital files can be copied infinitely. If I send you a digital photo, I still have it on my computer. So how do you prevent someone from spending the same digital coin twice?

Traditional systems solve this with a central ledger. A bank keeps track of who owns what, and prevents double-spending by checking the ledger before approving transactions.

Bitcoin’s solution: make the ledger public, shared, and cryptographically secured.

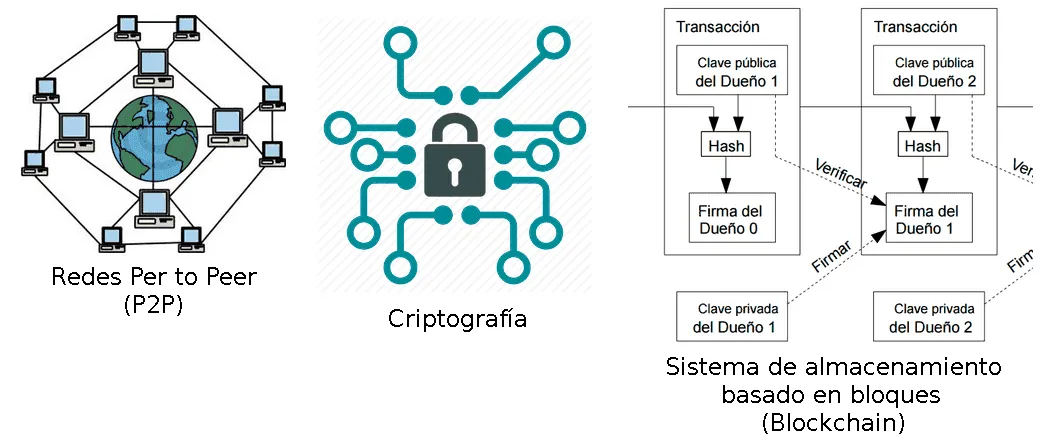

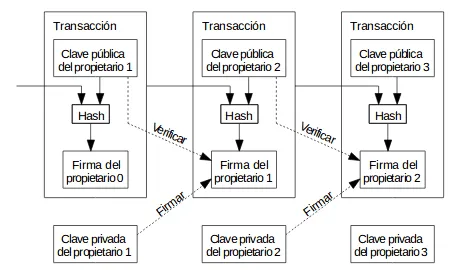

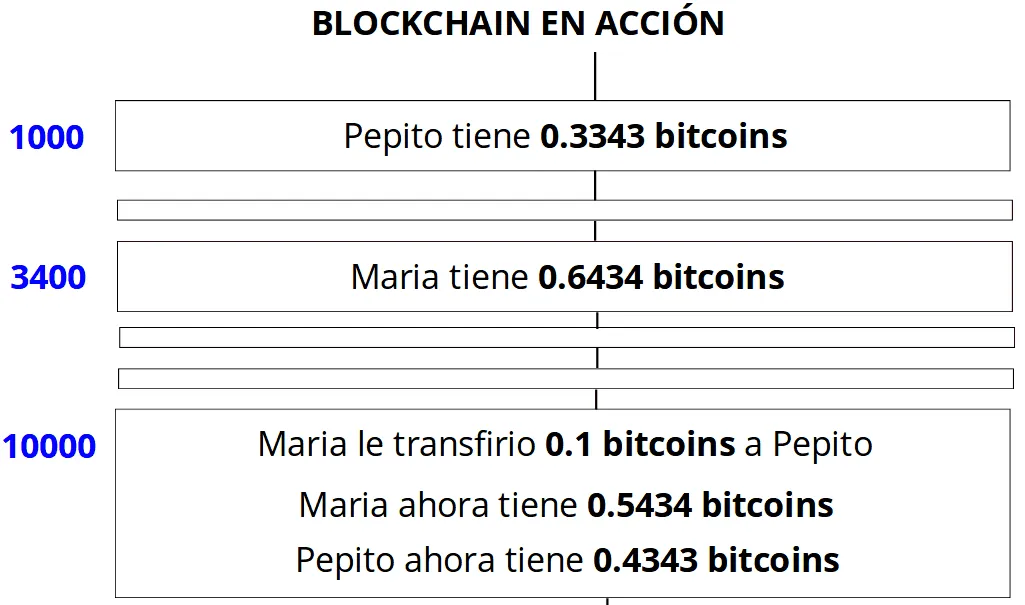

The Blockchain: A Chain of Digital Signatures

The blockchain is essentially a shared database — a ledger of all transactions ever made. But instead of being stored in one place, it’s distributed across thousands of computers worldwide.

Each block contains:

- A batch of recent transactions

- A timestamp

- A reference to the previous block

- A unique cryptographic signature (hash)

Blocks are chained together sequentially. Change one transaction, and the cryptographic signature changes. Change the signature, and the chain breaks. This makes it nearly impossible to alter past transactions without being detected.

Mining: Securing the Network

But who maintains this ledger? Who decides which transactions are valid?

That’s the job of miners — participants in the network who compete to create new blocks. Here’s how it works:

- Miners collect pending transactions into a new block

- They compete to solve a complex cryptographic puzzle (proof of work)

- The first miner to solve it broadcasts the new block to the network

- Other miners verify the block is valid

- Once verified, the block is added to the chain

- The winning miner receives a reward (new Bitcoin + transaction fees)

The proof-of-work system makes attacking the network extremely expensive. To rewrite the blockchain, you’d need to control more computing power than the rest of the network combined — and redo all that cryptographic work faster than honest miners are adding new blocks.

Satoshi compared it to gold mining: early on, gold is easy to find. But as time goes on, you have to dig deeper and work harder. Bitcoin mining works the same way — as more miners join, the difficulty adjusts to keep block times consistent (about 10 minutes per block).

Ethereum: Blockchain Meets Programmability

Bitcoin proved blockchain could work for money. But what else could you build on this technology?

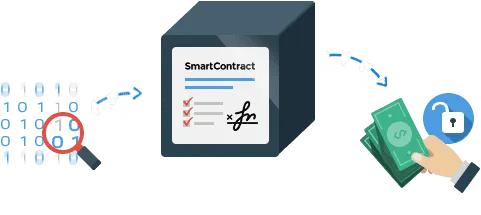

In 2014, Vitalik Buterin launched Ethereum — a blockchain platform designed for more than just payments. Ethereum introduced smart contracts: self-executing code that runs on the blockchain.

A smart contract is like a digital vending machine. You put in money, the contract checks if conditions are met, and if so, it automatically executes (sends you a soda, transfers ownership, releases funds, etc.).

This opened up entirely new possibilities. Now you could build applications on the blockchain — games, financial instruments, voting systems, supply chain trackers. These are called Ðapps (Decentralized Applications).

Beyond Bitcoin: The Industrial Revolution of the Internet

Here’s what excites me most about blockchain: it’s not just about money. At its core, blockchain is a shared database with built-in security and consensus mechanisms. You can store any kind of information in it.

For the first time, we have a way to transfer digital ownership without trusting a central authority. You can prove something happened, prove you own something, prove a record hasn’t been tampered with — all verifiable by anyone, anywhere.

Here are some of the most interesting applications I’ve seen:

Distributed Cloud Storage

Instead of storing files on Dropbox or Google Drive (centralized companies), projects like StorJ use blockchain to distribute files across a peer-to-peer network. Participants rent out their unused hard drive space in exchange for cryptocurrency.

Files are encrypted before being uploaded, so even though they’re distributed across many computers, only you can access them.

Internet of Things (IoT)

Billions of devices — sensors, smart appliances, wearables — will soon be connected to the internet. But securing low-power, low-cost devices is hard. Many IoT devices ship with weak security and never get updated.

Blockchain can serve as infrastructure for IoT communication — ensuring data integrity and enabling secure, automated interactions between devices through smart contracts.

Electronic Voting Systems

Electoral fraud is a massive problem worldwide. Electronic voting could solve it — but centralized systems can be hacked or manipulated.

Blockchain-based voting would be transparent, verifiable, and nearly impossible to tamper with. Projects like Polys, Secure Vote, and Voatz are working on this.

Digital Identity and Authentication

Right now, we have dozens of passwords for different services. It’s insecure and inconvenient.

Blockchain could enable a universal digital identity — a single cryptographic fingerprint you control. Use it to log in anywhere, prove who you are, and manage your personal data without relying on companies like Google or Facebook.

Medical Records

Your medical history could live on the blockchain — accessible to any doctor worldwide, yet fully under your control. Hospitals wouldn’t own your data. You would.

Tracking and Provenance

Blockchain lets you trace the history of any asset. Who owned this house before me? Is this diamond conflict-free? Is this artwork genuine? A blockchain-based registry provides an immutable, auditable history.

Gambling and Betting

Cryptocurrencies allow anonymous, instant, low-fee gambling. Smart contracts can automate payouts and ensure fairness — no trust required.

Digital Notary

Smart contracts could replace notaries for many legal agreements — automatically executing when conditions are met, with an immutable public record anyone can audit.

Why This Matters

Digital currencies will affect world finance, transform the way we pay for things, and perhaps make the world a fairer place. — Wall Street Journal (2015)

I’ve spent a lot of time thinking about blockchain — not just the technology, but what it represents. It’s a shift from trusting institutions to trusting mathematics. From centralized control to distributed consensus.

Will blockchain replace banks? Probably not entirely. But it offers an alternative — and alternatives are powerful. They force incumbents to compete, to innovate, to justify why they deserve our trust.

Blockchain is still young. The technology has scaling challenges, energy concerns, and regulatory uncertainty. But the core idea — a transparent, tamper-proof, decentralized ledger — is here to stay.

We’re still in the early days. But I believe we’re watching the foundation of something big being built.

References

- Blockchain Disruption (Coursera)

- Platzi: Bitcoin and Blockchain Course

- Blockchain: Beyond Bitcoin | José Juan Mora | TEDxSevilla

- Innovating with blockchain (TEDx Costa Rica - Nov 15, 2016)

- Documentary: Banking on Bitcoin (2016)

- Bitcoin: A Peer-to-Peer Electronic Cash System

- Basic Glossary on Bitcoin and Blockchain

- Brief History of Bitcoin

- Why Bitcoin Matters

Let’s keep building.